The housing market has experienced a notable power shift since the pandemic boom ended in 2022. While national inventory is still below pre-pandemic levels, the gap is narrowing. However, conditions vary dramatically by state, creating clear winners and losers for buyers and sellers. Here we answer key questions about the current state of inventory and what it means for your local market.

What is the current state of national housing inventory and how does it compare to recent years?

As of April 2026, active listings totaled 1,002,935 homes, up 4.6% year over year from 959,251 in April 2025. This is a significant recovery from the pandemic low of 379,978 in April 2022, but still 11.8% below the pre-pandemic level of 1,137,198 in April 2019. Inventory has been steadily climbing since 2023, though the pace of growth has slowed. For context, the year-over-year increase was 30.6% just 12 months prior. If current growth continues at the same rate (about 43,684 additional homes per year), inventory could reach 1,046,619 by April 2027, but that is not a prediction—just a projection based on current math.

Why are active listings and months of supply critical for understanding market power?

Active listings and months of supply are leading indicators of pricing momentum. When inventory rises rapidly and homes linger on the market longer, sellers may need to cut prices, signaling a buyer's market. Conversely, a sharp drop in inventory, beyond normal seasonal patterns, gives sellers leverage to demand higher prices and less negotiation. Since the national pandemic housing boom fizzled out in 2022, the balance has gradually tilted from sellers toward buyers, but with wide regional variation. Monitoring these metrics helps predict which local markets are likely to see price softening or continued strength.

How has the buyer-seller power dynamic shifted since the pandemic boom ended?

From 2020 to 2022, sellers dominated as inventory plummeted to historic lows—active listings hit just 379,978 in April 2022. Since then, inventory has more than doubled, giving buyers more options and negotiating power. This shift has been directional but uneven: some markets have seen inventory surge well above pre-pandemic 2019 levels, leading to softer home price growth or even declines. In contrast, areas where inventory remains far below 2019 levels have experienced more resilient price appreciation. Nationally, the market is still below 2019 levels, so the power balance hasn't fully swung to buyers, but the trend is clearly moving in that direction.

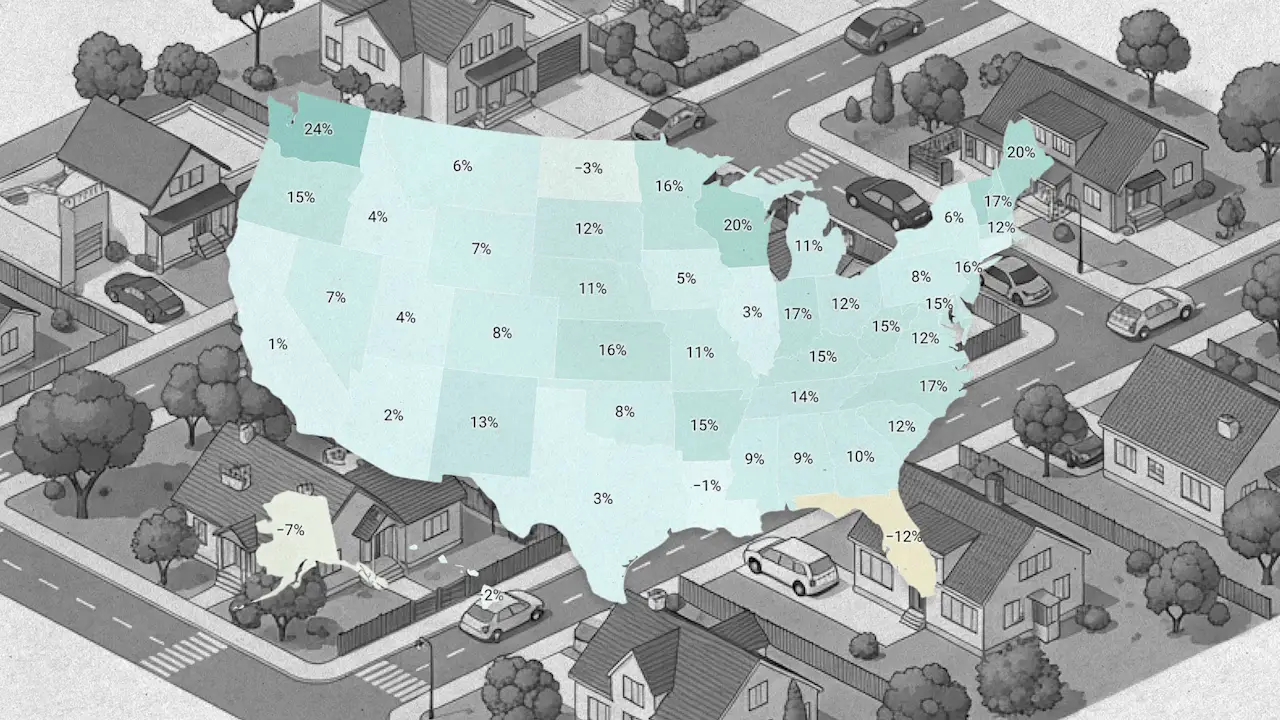

Which states have inventory levels above pre-pandemic 2019, and what does that mean for buyers?

States where active inventory has recovered to or exceeded 2019 levels—typically in the Sun Belt and parts of the West, such as Florida, Texas, Arizona, and Idaho—tend to favor buyers. In these markets, more supply means less competition, longer days on market, and greater likelihood of price reductions. Sellers may need to offer concessions or accept lower offers. This does not guarantee a crash, but it does soften price growth and can create opportunities for buyers who have been sidelined. However, even in these states, local variation exists, so it's important to drill down to city or neighborhood data.

Which states have inventory far below 2019 levels, and how does that affect prices?

Many markets in the Northeast and Midwest—such as Massachusetts, New York, Illinois, and parts of the Ohio Valley—still have active listings well below pre-pandemic 2019 numbers. This scarcity gives sellers the upper hand, leading to bidding wars, faster sales, and resilient price growth. Even though national inventory is rising, these local shortages mean buyers face limited choices and higher costs. For sellers in these regions, the market remains strong, though they must price competitively as conditions evolve. The tightness in these areas is a key reason national inventory remains below 2019 levels overall.

What has been the year-over-year trend in inventory growth recently, and is it slowing?

From April 2024 to April 2025, national inventory grew by 30.6%, a rapid increase. However, in the most recent 12 months (April 2025 to April 2026), the growth rate slowed sharply to just 4.6%. This deceleration suggests that the initial post-pandemic inventory recovery is maturing. The market may be nearing a new equilibrium where supply stabilizes rather than continues to surge. For homebuyers, this means the window of rapidly improving choice may be closing, though inventory is still rising. For sellers, the slowdown in new listings could reduce competitive pricing pressure, particularly in markets that are still tight.

What does the future look like for housing inventory under current trends?

If the current pace of adding about 43,684 homes per year persists, inventory could reach roughly 1.05 million by April 2027, still below the 2019 baseline. However, many factors could shift this trajectory: mortgage rates, new construction, and economic conditions. The slowdown in year-over-year growth suggests the market is adjusting, not booming. In states where inventory already exceeds 2019 levels, further increases may be modest. In tight markets, building more homes will be key to easing supply constraints. Overall, the national market is moving toward balance, but a true buyer's market may remain elusive in many regions for years to come.